Whether investing or saving, the first and most important thing for you to understand is that you should start as early as possible. Both saving and investing are done to preserve and grow our capital, and time plays a vital role in how greatly it will compound.

So let us first understand these terms as they can often be used interchangeably, and in general, language has a minute difference.

Saving - The practice of putting money in things like a savings account or a fixed deposit is generally considered as savings. The critical factor here is that these instruments assure the safety of capital and provide a fixed rate of return on the invested money.

Investing - The practice of putting money in riskier investments like the stock market, mutual funds, gold, etc., is considered to be supporting. The critical factor here is that these instruments promise higher returns but come with a particular risk.

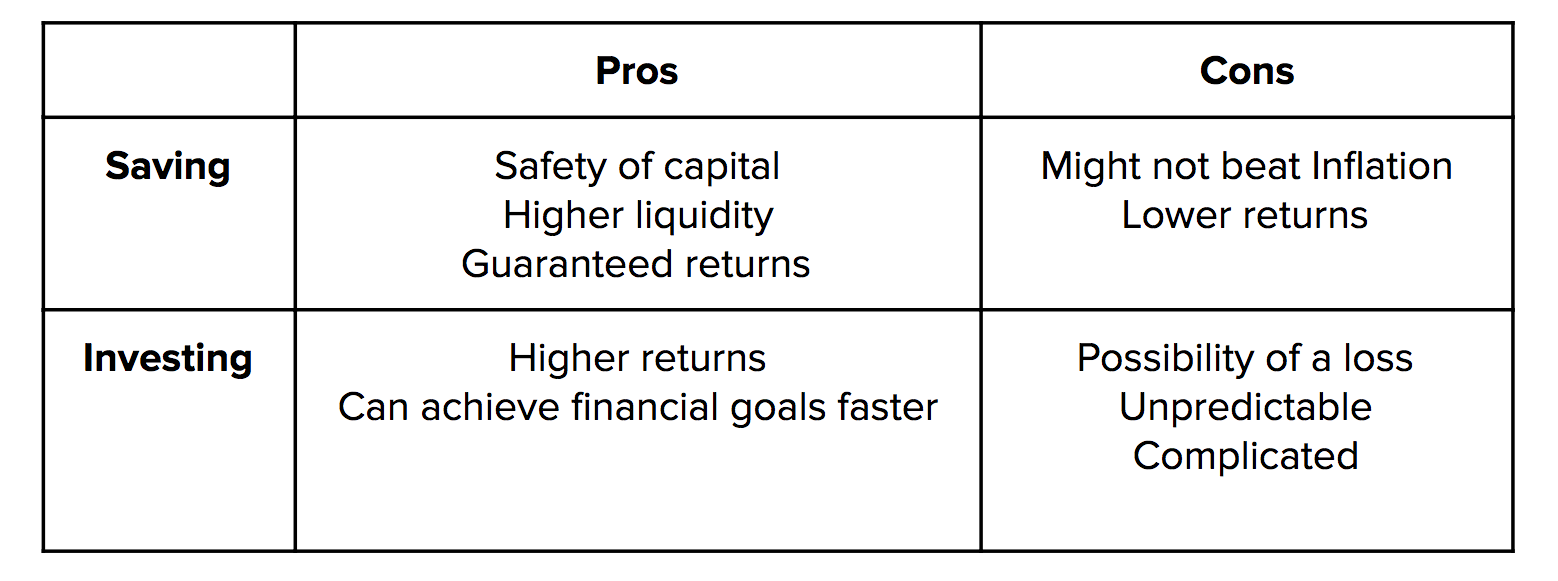

Let us look at the Pros and Cons of both saving and investing:

Read more: Liquid Funds vs Fixed Deposits: How To Make The Right Choice

As you must have understood from the table, people who are looking for safety of capital and are happy with lower returns should focus on saving. In comparison, the ones who do not mind assuming the higher risk for the possibility of better returns should focus on investing.

One important thing to understand here is that the two are not binary, and you should do both at all times. For example, the money you save for your emergency fund should be your savings and invested in a fixed deposit or a savings account. However, the money you save for your investment fund should be invested in a diversified portfolio of different investing instruments like mutual funds, bonds, gold, index funds, etc.

So first and foremost, you should begin by analyzing your financial well-being. You need to take care of a few things before you can start investing.

- Pay off Debt - If you have outstanding debt, you should pay it as soon as possible. After you have cleared all debt, you should think about investing in riskier assets.

- Build an Emergency Fund - This is the first kind of saving you should do as soon as you get rid of your debts. The money in this fund should be invested in a savings account or a fixed deposit.

- Buy Insurance - Do not underestimate the risk of things not going as planned. Buy term life insurance and health insurance as early as possible in life.

Read more: What Is Debt-To-Income Ratio and Why Is It Important?

Once you have these three things covered, you can start thinking of investing. While you are investing, you might want to add a little bit towards your emergency fund and save some money in safer assets like a public provident fund.

Ultimately your investment portfolio should be well-diversified and should account for as many kinds of risks as possible. You must understand your financial goals and plan your investments accordingly.

For example, if you have a short-term goal, you should save safer assets like a savings account or a fixed deposit. However, if you plan for a long-term goal like retirement, you can invest in riskier assets like equities and mutual funds. It would be best if you also remembered that as you get closer to your long-term goal, you should modify the proportion of your money that you invest in savings and invest in inequities.

To conclude, begin by assessing your financial situation and follow the correct process. Plan your goals and save accordingly. Divide your savings into risk-free and risky investments based on your goals and financial backup. Do not underestimate risk and begin as early as possible!

(Check out 'Learn & Grow with Wizely' 'to read and learn all about personal finance and financial planning.)